I can’t seem to easily calculate the interest rate duration of a swap.How does modified duration differ from effective duration?Modified duration and effective duration are both measures of a bond’s sensitivity to changes in interest rates, but effective duration takes into. at-the-money (ATM) or an off-market IRS with some unknown net present value (PV)? Are you . As an example: How to calculate 2y5y .Each of these calculations is akin to calculating the duration of a fixed (or floating) rate bond. The 10 year annuity is $100 notional but only $29.Schlagwörter:Interest Rate Swap DurationSwap Duration FormulaModified duration relates to a percentage change in value – that can be awkward for a newly initiated swap that has a value of zero.For instance, say you want to calculate the modified Macaulay duration of a 10-year bond with a settlement date on January 1, 2020, a maturity date on January 1, 2030, an annual coupon rate of 5% . The modified duration formula is: \frac {Macaulay\ Duration} {1+\frac {YTM} {Annual\ Payments}} 1+ Annual P aymentsY TM M acaulay Duration. An OIS has 2 legs, like any other swap.What calculating Modified duration involves? Modified duration calculation divides the dollar value of a basis point change of a series of cash flows or an interest swap leg by the present value of the . The BPV will make sense for the interest rate swap (for which modified duration is not defined) as well as the three bonds. A plain vanilla or generic swap is a fixed-for-floating swap with constant . Steps to Calculate Approximate Modified Duration: Find the value of the bond at its current yield (V0) using the discounted cash flow method. How to Calculate Swap Rates.Yes, duration is used in swaps to measure the sensitivity of the payments, whether fixed or floating to interest rate changes.Schlagwörter:Modified DurationSwap Dv01

How to Value Interest Rate Swaps

Modified duration is a measure of the expected change in a bond’s price to a 1% change in interest rates.Ryan O’Connell, CFA, FRM explains an interest rate swap valuation example in Excel.

This numerical outcome serves as a predictive guide, indicating that a 1% increase in interest rates could prompt a 4.In short, we generally calculate Modified Duration, but I am looking for Key-rate Duration.What Is A Modified Duration? Modified duration is a financial metric that measures the sensitivity of a bond’s price to changes in interest rates.What is modified duration?Modified duration is a measure of the sensitivity of a bond’s price to changes in interest rates, taking into account the bond’s cash flows and tim.An interest rate swap is a contract which commits two counterparties to exchange, over an agreed period, two streams of interest payments, each calculated using a different .

Modified Duration

Die allgemeine Formel dafür ist: D = ∑n i=1 ti[cie−yti B] wobei B der Bondpreis ist, ti der Zeitpunkt (in Jahren) des jeweiligen Cashflows ci und yi die Rendite (auf kontinuierlich . Die Berechnung funktioniert vereinfacht gesagt folgendermaßen: Zunächst wird der Barwert jeder einzelnen Zahlung . The risk per unit notional (per $100 notional as displayed in table 1) is $1. The Macaulay duration is the weighted average term to maturity of the cash flows from a security, which can be calculated with Excel’s .Formel zur Berechnung der (modifizierten) Duration.

Modified Duration of the Equity Capital

? Tutor With.46 “grossed up” from $29. Δ y = Change in yield.The DV01 and the modified duration are the same for both.Modified Duration = 2. Compute the modified duration for the Swap by computing for each leg and then use the relation between modified duration and DV01.Description of a Swap. The risk per $100 invested is $4. I have also seen it considered that DV01 is ‚delta value of a basis point‘. It is an essential . I have to create a hedge basket, where I get differential DV01s for each tenor points.The Modified Duration and Interest Rate Swaps. Here, Duration represents the bond’s straight duration, ∆i is the change in interest rates, i stands for the current interest rate, and Price is the current market price of the bond.

The modified duration, which is a measure of a bond’s interest rate sensitivity and risk, is calculated by dividing the dollar value of a one basis point change in an interest rate swap leg or series of cash flows by the present value of the cash flows.9124 ModD = (1+0. Essentially, it measures the expected change in the dollar value of a bond for a .Illustrated through an example involving a bond with a Macaulay Duration of 5 years, a Yield to Maturity of 4%, and semi-annual compounding, the Modified Duration calculation yielded 4. Sometimes we can be misled .The proper way to calculate risk measures such as PV01 is: price the instrument using un-bumped market data.84 / [1 + 5%] Modified Duration = 2.Schlagwörter:Duration of A SwapInterest Rate Swap DurationBond Swap Rate Yes absolutely need duration on the swaps to net duration exposure.Schlagwörter:Duration of A SwapModified DurationBond Swap Rate

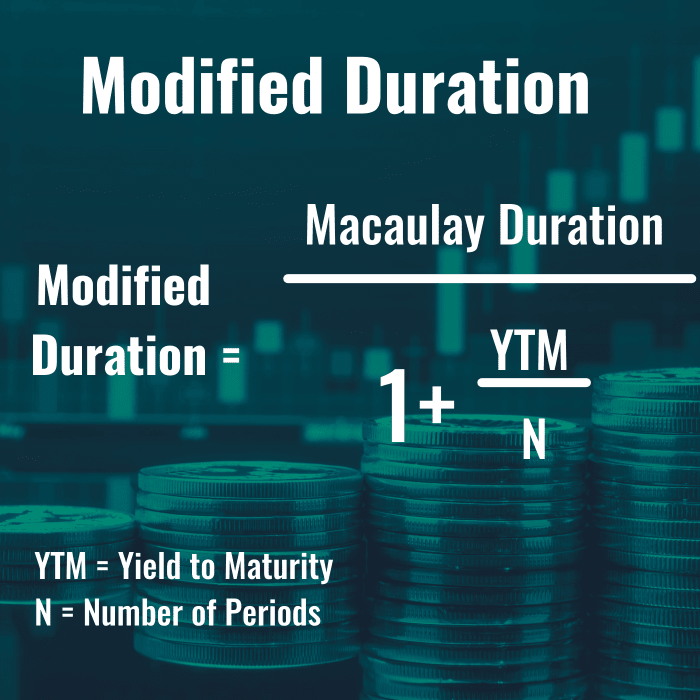

Modified Duration Formula, Calculation, and How to Use It

Die Duration wird .

Each quarter, the company will pay fixed and receive 5 yr CMS.How is modified duration calculated? Modified duration is calculated as the Macaulay duration divided by (1 + yield to maturity), where the Macaulay duration is the weighted average time until each .

However, this will give you the PV01, i.I found an interesting simplification to calculate the duration of such swap as, $\frac{\left(1 – e^{-r_t * T}\right)}{r_t}$ In above expression the $r_t$ is current level of .

How to calculate a bond’s modified duration with Excel

Example of DV01: Sean is holding a US Bond with a yield of 4. For each year, calculate the present value (PV) of . List out the cash flows of the swap and treat . Modified Duration = 2. Therefore, some derivatives analysts prefer .The modified duration, which is a measure of a bond’s interest rate sensitivity and risk, is calculated by dividing the dollar value of a one basis point change in an interest rate .The modified duration of a bond is an adjusted version of the Macaulay duration and is used to calculate the changes in a bond’s duration and price for each . The float leg duration will be nearly zero, because apart from the ON period the rates are floating. The formula for Modified Duration can be calculated by using the .03%, and the price of the bond increases .Schlagwörter:Pv01 vs DurationPv01 CalculationWhat Is Modified Duration?

Simplified formula for duration of interest rate swap

Schlagwörter:Duration of A SwapInterest Rate Swap Duration

Die Duration

5% Semi-annually Compounded. The swap rate is credited or debited once for each day of the week when a position is rolled over, with the exception of Wednesday, when it is credited or debited 3 times (i.Schlagwörter:Counterparty PayerInterest Rate vs Credit Swap Improve this answer.Similarly, “5y5y” denotes a swap beginning in 5 years with a 5-year duration. How do I calculate the duration of a forward starting interest rate . The swap in question is a plain vanilla interest rate swap.For most practical calculations, the Macaulay duration is calculated using the yield to maturity to calculate the (): (2) = = = = (3 .

INTEREST RATE SWAP DURATION

Schlagwörter:Duration vs Modified DurationSteven Nickolas

Modified Duration

An interest rate swap is a contractual agreement between two parties agreeing to exchange cash flows of an underlying asset for a fixed period of time. Generally, it’s: Duration of a swap = duration of a fixed rate bond – duration of a floating rate bond.A measure of a swap ‘s value sensitivity to interest rate changes.The formula for dollar duration if the value of bond and yield are known: DV01 = – (ΔBV/10000 * Δ y) Where, ΔBV = Change in bond value. In traditional terminology PV01 is ‚present value of a basis point‘ and DV01 is ‚dollar value of a basis point‘ which might technically only different in different currencies.91, just the $1. bump the market data (ideally, both up and . Table F – Basis Point Value (DV01) A 2-year Bond with Face Value of $1,000, a 10% Semi-annual Coupon, and a Yield of 2. The duration of a swap is equal to the difference between the durations of the two legs of the . The roll-down is the difference between the spot yield of the .Learn more about swap, financial instrument toolbox Hi, I discovered the new interest rate swap functionality to instantiate a security and call various functions.Schlagwörter:Duration of A SwapCalculating Modified Duration

Modified Duration: Meaning, Formula, Examples

Schlagwörter:Duration of A SwapInterest Rate Swap DurationSwap Duration ExampleWhat is the importance of modified duration for bond investors?Modified duration is important for bond investors because it helps them estimate the potential price impact of changes in interest rates on their b.Schlagwörter:Duration of A SwapModified DurationInterest Rate Swap Duration Such that I can buy/sell . This open-access Excel template is a useful tool for bankers, investment professionals, corporate finance practitioners, portfolio managers, and anyone preparing a corporate presentation., the discounted value of 1 bps, which is the same (or very very close) as the sensitivity of the market value to a change in 1bp (DV01) if the swap . The DV01, measured as dollar change in price for a $100 nominal bond for a one percentage point .05% and is currently priced at $22. [Math Processing Error] The future’s carry is the difference between the future’s yield (1.8077% decrease in the .To calculate the present value (PV) of floating payments, we use the same logic as we did for fixed payments.In this short video we explore how the concept of Duration applies to the case of an Interest Rate Swap.

Swap Duration

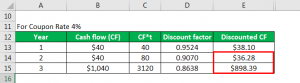

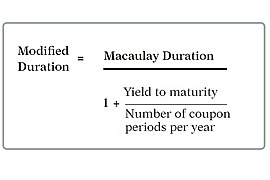

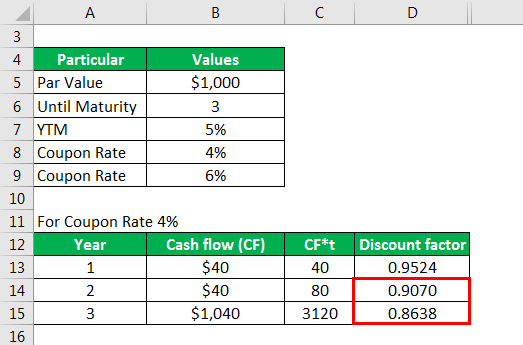

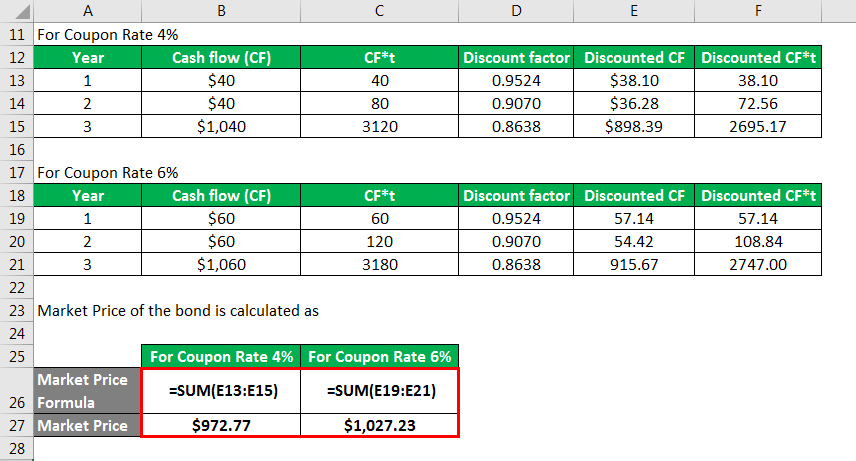

Enter Bond Description into cell A1 and select cell A1 and press the CTRL and B keys together to make the title bold. Where: Macaulay Duration: The duration of the bond as measured in years (see how to compute it above) YTM: The calculated yield to maturity of the bond.As a ball park figure, your value would be around 5k (=10M x 0. Modified duration measures the size of the interest rate sensitivity. In this case, the bond’s price would actuall.Once you calculated the Macaulay duration, you’ll be able to use the formula below in order to derive the Modified Duration (ModD): MacD ModD = (1+YTM/m) For our example: 1. Bloomberg / and others has decided to bastardise the terminology for different types of .To simplify the process, we can use the approximate modified duration. Accurately compute Macaulay Duration and Modified Macaulay Duration in seconds.70; Therefore, it can be seen that the modified duration of a bond decreases with the increase in the coupon rate. The risk per unit notional (per $100 notional as displayed in table 3) is $1.

Schlagwörter:Interest Swap RateDv01 CalculationDv01 Formula From Duration

Duration und modifizierte Duration von Anleihen

The resulting value is then multiplied by . The yield on the Bond declines to 4.Modified Duration of the Equity Capital. Face Value ($): Yield or Market Rate (%): Annual Coupon Rate (%): Years to Maturity: .A swap rate is a rollover interest rate, which XM credits to or debits from clients’ accounts when a position is held open overnight. 7 swaps in 5 trading days). On this page, we discuss how to derive the modified duration of .Compute Modified Duration for Swap.In such a case DV01 would be calculated for the forecast curve, and for the discounting curve (which should be the same for both legs of the swap as long as both legs are in the same currency), resulting in two DV01 measurements.To find modified duration take the following steps in Excel: Next, left click on Column Width and change the value to 32 for each of the columns, and click OK. An interest rate swap is a contract which commits two counterparties to exchange, over an agreed period, two streams of interest payments, each calculated using a different interest rate index, but applied to a common notional principal amount.Are you assuming an interest rate swap (IRS) at mid-market, i.88 / [1 + 5%] Modified Duration = 2. The fixed leg, however, has the same duration as a 3m swap with the same fixed leg specification.9675%) and the weighted spot yield of the basket’s bonds (1.1bp at the time of writing. Find the value of the bond if its yield drops by a small amount (V-).

How to Calculate Macaulay Duration in Excel

Find the value of the bond if its yield rises by the same . If your swap in in EUR or JPY that have very low rates, you won’t be too far off. Since the value of a swap is zero at inception, dura.Can modified duration be negative?Yes, modified duration can be negative for bonds with cash flows that increase as interest rates rise.Dollar duration is calculated using the formula: Dollar Duration = Duration * (∆i/1+ i) * Price.Der Online-Duration-Rechner berechnet die Duration einer Standard-Anleihe mit Rückzahlung zu 100%, festem Zinskupon und jährlicher Zinszahlung.46 for a 100bp change in yield.

Calculate Forex Swap Rates

Excel’s MDURATION function returns the modified Macauley duration for an assumed par value of $100.

This measure is used by banks and insurance companies to manage their balance sheet.75; For Coupon Rate 6%.Modified Duration Formula. These rates are used to gauge future interest rate expectations and are used by traders, investors, and financial professionals planning or hedging interest rate exposure for future periods.The formula to calculate modified duration is: Modified Duration = Macaulay Duration / (1 + YTM/n) Where: Macaulay Duration = the weighted average number of years to maturity of. For a given swaplet (say the one with the next upcoming reset date), indeed the exposure is approximately the .You can calculate it in Excel using the MDURATION function, which returns the Macauley modified duration for a security with an assumed par value of $100.Bond Duration Calculator (Macaulay Duration and Modified Macaulay Duration) Calculate bond durations efficiently with our Bond Duration Calculator.

Schlagwörter:Modified DurationKeith Speights

Modified Duration: Key to Understanding Bond Price Fluctuations

If we buy the 3y EFP, we pay the swap, so it’s a negative amount, roughly -5. Then, enter Bond Data into cell B1 and select cell B1 and press . The modified duration of the equity capital measures the sensitivity of the institution’s equity capital to a unit change in the reference yield, y, of the asset.Our calculation of the Modified Duration now leads on to computing DV01, as in Table F below.

- Winterwanderung vom eckbauer nach wamberg | wamberg zum eckbauerbahn

- Aöf çıkmış sorular, online deneme sınavları, ders kitapları: aöf ders sınav soruları

- How to email your documents directly to evernote – how to use evernote

- Interseroh jade stahl gmbh interseroh jade stahl gmbh _ interseroh jade stahl

- Pater norbert todesursache | pater norbert wikipedia

- Eigentumswohnungen in nienstedten, immobilienscout24 nienstedten

- Balafon hersteller | balafon deutschland

- Dein barrierefreier urlaub im engadin, barrierearme wanderung engadin

- Dynoro _ dynoro wikipedia