Geschätzte Lesezeit: 10 min

Margin Calculators

For listed derivatives, CDS, IRS, and OTC JGB, open positions are marked-to-market using the most recent price at least once a day, following which variation margin is . PBN01 contains all Special Repo transactions and all GC Pooling transactions excluding the GC Pooling Equity Basket.What the models for computing margin requirement for central counterparty (CCP) and non-central cleared OTC derivatives.Initial Margin (IM) is the amount of collateral required to open a position with a broker or an exchange or a bank.

Risk Management

The information furnished is with no warranty as to accuracy or completeness of its contents and on condition that any changes, omissions or errors shall not be made the basis for any claim, demand or cause of action.

Total Initial Margin information is available in the Financial Resources section of ICE Clear Europe’s Regulation webpage. The margin requirement for the portfolio is set at a .0, became effective in December 2017 to include a range of clarifications, enhancements and additional risk . Unlike the dealers who need to have a comprehensive understanding of the new margin rules, . Initial margin represents one of the . The margin mode of any position or open order cannot be changed. Margin is computed by stress testing the portfolio in a range of simulated market conditions. According to Principle 6 of the PFMI, initial margin for derivatives should meet an established single-tailed confidence level of at least 99% with respect to the estimated d.n period of risk (“MPOR”). Collateral Margins can be posted in cash or in liquid government bonds issued by sovereigns with low credit risk.

Documentation & installation guide for CME PC-SPAN software & CME SPAN Risk Manager software. The picture at the bottom of my post may be helpful for you.

Net Interest Margin (NIM)

This presentation provides an overview on the concept of margining at ECC, its different types and calculation methods.Initial Margin Calculation Guide Page 4 of 36 1.

CCP12 PRIMER ON INITIAL MARGIN

Dateigröße: 995KB Access portfolios from the two Margin Calculators– Rates or FX and F&O. Initial margin is a returnable deposit based on .The Initial Margin requirement is currently calculated using ICE Risk Model 1 (IRM 1). Backtesting of SIMM over a historical period and Benchmarking of SIMM against the industry standard risk models to cover the Model Governance requirements. The Simm officially launched in September 2016 and an updated version, Isda Simm 2.In order to facilitate the introduction of final BCBS-IOSCO guidelines for “Margin requirements for non-centrally cleared derivatives”, published September 2, . The information in this presentation serves for . Posted government bonds are marked to market on a daily basis, using prices or quotes made available by info providers, and are grouped in classes of duration, each .

Standard Initial Margin Model for Non-Cleared Derivatives

At Eurex Clearing we understand that sophisticated margin replication and calculation is important for our members and their clients. Under new margin rules for non-cleared derivatives, in-scope entities need to exchange initial margin on most non-cleared derivatives, but delays and disputes can . Discounts are set by the broker, however they cannot be lower than the exchange set values.Margin calculator is a tool only and margin numbers are indicative in nature.Margin Calculators. (As of December 18, 2023) JSCC requires Clearing Participant to deposit margin, which is collateral to cover loss arising from that Clearing Participant default.The new calculation method is intended to shore up protections for both investors and clearing brokers by controlling sharp fluctuations in margin levels and improving risk management.This methodology allows ECC to align margin requirements with risk, thereby realizing efficient margining. futures and options on BTC and ETH.For Default Management purposes (auctions and default fund segmentation) the additional Bond Liquidation Group PBN01 is defined.As a starting point for the initial margin calculation, the model requires firms to calculate sensitivities in accordance with ISDA SIMM™ for all in-scope trades.If an account is in portfolio margin mode, you would be able to trade only those contracts in this account that support portfolio margin mode, i.Material swaps exposure for an entity means that, as of September 1 of any year, the entity and its margin affiliates have an average month-end aggregate notional amount of uncleared swaps, uncleared security-based swaps, foreign exchange forwards, and foreign exchange swaps with all counterparties for March, April, and May of that .

SPAN Margin: Definition, How It Works, Advantages

considers both initial margin (IM) and variation margin (VM), centrally and non-centrally cleared markets (including clearing member-client dynamics), margin practice . This can be a significant data exercise in itself. The box model stands for the four edges forming the body document: the margin area, border area, padding area and content area. ribution of future exposure.

Margin Methodology

p end users navigate the uncleared swap margin rules. Download the latest version. Currently Eurex Clearing applies two margining methods .

Margin Calculation: Exchange Model

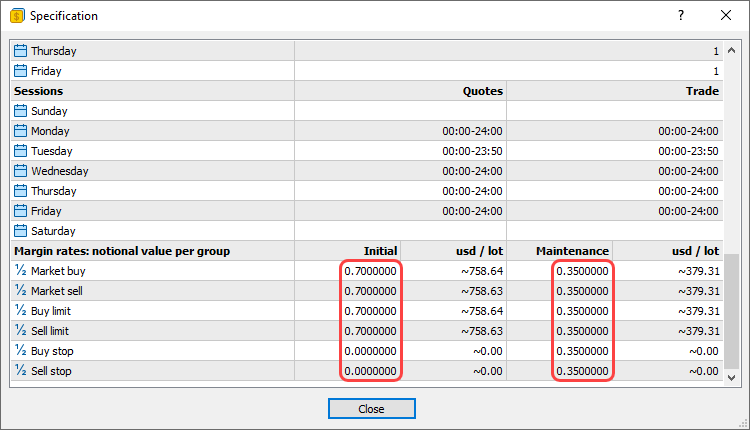

The margin for the Forex instruments is calculated by the following formula: Volume in lots * Contract size / Leverage. ECC’s target model is the Prisma methodology, initially developed and deployed by Eurex Clearing AG.Perhaps you’ve read about the Black-Scholes Model but wonder where it comes into play in the world of options trading. Margin calculation is based on the discounts for instruments. Initial margin calculation is counterparty .The aim of the Nord Pool Margin Model is to produce a collateral requirement that easily and realistically reflects the risk in a member’s trading behaviour. Learn more about the margining methodology.CME SPAN Methodology Resources.This page is about New Margin Calculation Method (VaR Method).

Because of this, CCPs and Exchanges are moving away from SPAN to VaR -based methodologies for margin calculation, for example: Eurex have already made . Margin Requirements (Ags, Index, Metal & Currency Products)

Nasdaq Clearing Margin Methodology & System Requirements

Margin Optimization is available from the Rates Calculation screen. INTRODUCTION Hong Kong Securities Clearing Company Limited (“HKSCC”) adopts VaR Platform to determine the initial margin (“IM”) requirement of Clearing Participants’ (“CPs”) portfolios.

Initial Margin Preparation Guide

Developed by the Chicago Mercantile Exchange (CME) in 1988, SPAN ? calculates margin based on 16 highly simplified . Trades need to be identified as being in-scope, labelled correctly and appropriate sensitivities must be calculated for each trade.ICE Risk Model 2 (IRM 2) is the new initial margining (IM) model developed by ICE to replace the existing ICE Risk Model (IRM 1) for exchange traded futures and options.

Learn more and see examples. Customize your inputs or select a symbol and generate theoretical price and Greek values. All disputes with respect to the distribution activity, would not have access to Exchange investor redressal forum or Arbitration .Wir von Eurex Clearing verstehen, dass eine ausgefeilte Margin-Replikation und -Berechnung für unsere Mitglieder und deren Kunden wichtig ist. Using 16 scenarios, the CME SPAN Methodology can assess risk for futures, options, physicals and equities.The ICE Risk Model is used at most of ICE’s clearing houses to calculate futures and options margin on at least a daily basis. This means that if you wish to activate portfolio margin for an account, you must not have any open positions or . Initial margin is the minimum value of trader’s own funds with which the trader is allowed to enter the market.

Standardized Initial Margin Model

What Is Span Margin? ECC is planning to replace the current SPAN1 initial margin model for derivatives with a portfolio-based initial margin model. For this purpose we offer applications designed to help calculate and simulate margin requirements at Eurex Clearing.The lending business model of a bank or financial institution is oriented around structuring debt products, such as loans and . No more taking trades just to figure out the margin that will be blocked!Geschätzte Lesezeit: 7 min

Margin Calculation: Exchange Model

Intraday margins are calculated the same way as end of day margins.

It is designed to provide a common methodology for calculating initial margin for uncleared .ICE Clearing Analytics (ICA) is ICE’s new web-based platform for calculating ICE Risk Model 2 initial margin (IM) and related margin add-ons.How to Use This Handbook. Skip to main content.Currently two models for the calculation of initial margins for bilateral derivatives are available: has been defined by the regulators and is straight-forward to implemen. Initial Margin is a.SIMM stands for Standard Initial Margin Model for non-cleared derivatives. ECC updates the SPAN® risk parameters daily. This tool is for informational purposes only. The technical platform including member interfaces will be the state-of-the-art Risk Management .Eurex Clearing Margin Calculators. Exchange files and other data. Eurex Clearing Margin Calculators.The Standard Initial Margin Model (SIMM) is very likely to become the market standard.MarginCalculator – Guided Tour

Fehlen:

exchange model

SPAN Vs VaR

The ISDA Standard Initial Margin Model (ISDA SIMM ®) is an industry standard methodology for calculating regulatory initial margin for non-cleared derivatives.The model applies a sensitivity-based calculation across four product groups: interest rates and foreign exchange (ratesFX), credit, equity and commodities. This is a legal liquidation group and has no impact on margining.

Margin Calculation for Retail Forex, Futures

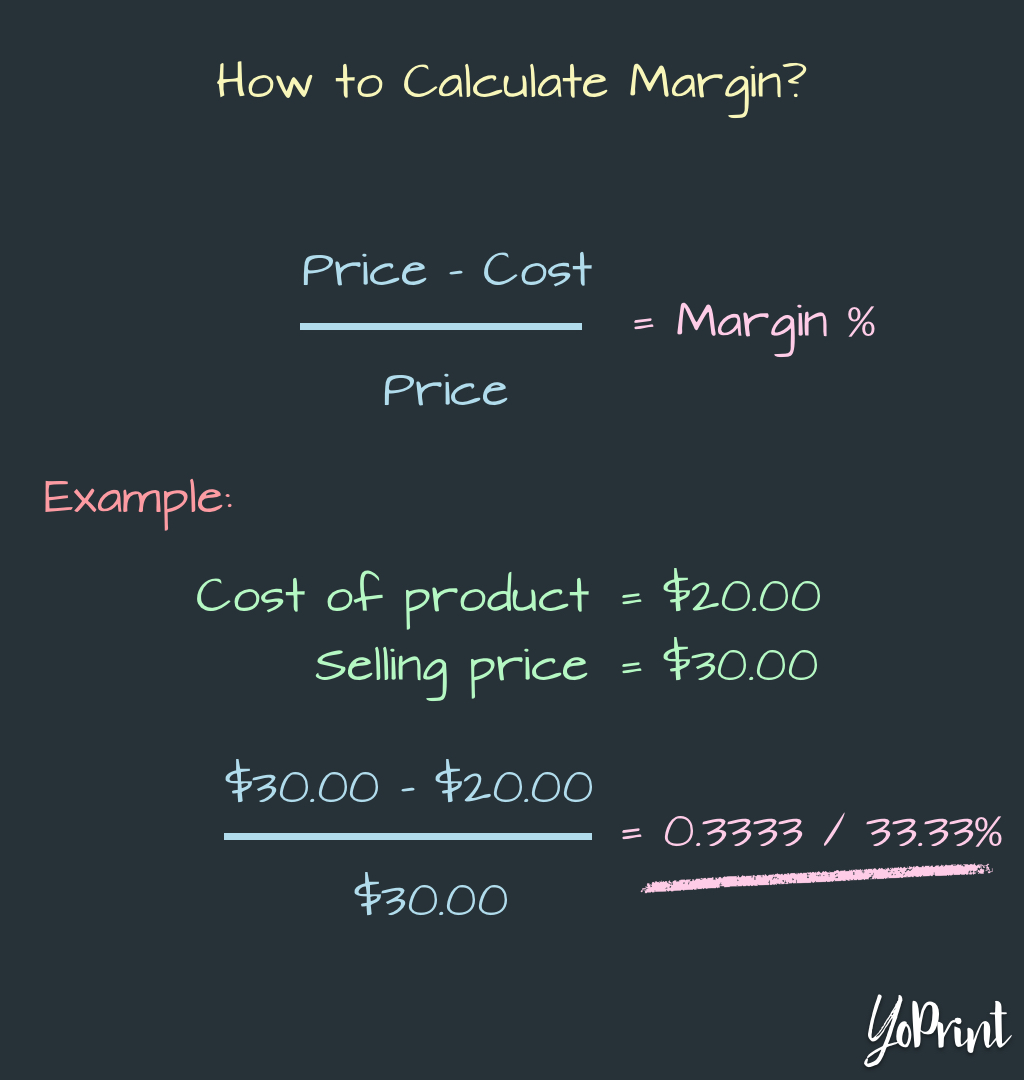

ICE Clear Europe will start migrating to ICE Risk Model 2 (IRM 2) in 2024.Self-Regulatory Organizations; The Options Clearing Corporation; Notice of Filing and Immediate Effectiveness of Proposed Rule Change by The Options Clearing .The calculation method of this initial margin aims at ensuring market safety while reducing the costs for financing operations on the market.The commencement of JSCC’s Clearing Business combined the clearing of cash transactions, which used to be handled by each exchange, and dramatically improved the safety and efficiency of the clearing and settlement processes.Margin calculation methodology.Our margin requirement systems calculate accurate risk-based margin requirements for each counterparty account. These are not Exchange traded products, and the Member is just acting as distributor. These parameters . The padding area extends to the border surrounding the padding.For Stock Exchange, based on margin discount rates — used for the exchange market.As inputs to the portfolio calculation, Nodal Clear’s margin methodology employs return observations from recent trading activity (past one to three years) and return . For information about ICE’s new risk model, please see here. The model estimates a .Learn about gross, operating, and net profit margins, how each is calculated, and how businesses and investors can use them to analyze a company’s profitability. It is designed to provide a common methodology for calculating initial margin for uncleared OTC derivatives. The Standard Initial Margin Model (SIMM) is very likely to become the market standard.

Fehlen:

exchange model Another component is the MPOR or the closeout period that a CCP assum. At Eurex Clearing we understand that sophisticated margin replication and calculation is important for our members and . Stack Exchange network consists of 183 Q&A communities including Stack Overflow, the largest, most trusted online community for developers to learn, share their .How to Calculate Net Interest Margin? The net interest margin is a measure of profitability in the financial sector, which comprises financial institutions such as commercial and corporate banks and other lenders. The Zerodha F&O calculator is the first online tool in India that let’s you calculate comprehensive margin requirements for option writing/shorting or for multi-leg F&O strategies while trading equity, F&O, commodity and currency before taking a trade. Adjusted initial margin is the minimum value of trader’s own .To help address these needs, we provide: Accurate Risk Sensitivities and Initial Margin calculations using the ISDA Standard Initial Margin Model (ISDA SIMM TM) and Schedule based models.Margin Calculator – Get free online calculator for calculating Span Margin required for initiating a trade in the market at Upstox. Stack Exchange Network.

Clearing Margin Models

The model contains portfolio margin component for Primary Tier (“Tier P”) instruments, flat Zu diesem Zweck bieten . The options calculator is an intuitive and easy-to-use tool for new and seasoned traders alike, powered by Cboe’s All Access APIs. Yes, the box-model includes the margin. It is a method for calculating the appropriate level of initial margin (IM) for non-cleared derivatives; where IM is essentially a reserve for potential future exposure (PFE) during a margin period of risk (MPR), capturing funding costs.The research results show that the company’s profit which is projected with a contribution margin has a positive effect on dividends and Return on Investments has a positive effect on return and contribution margin and return on investment has no effect on dividends, and this is in accordance with the R square result of only 3.

- Rtl aktuell im stream heute live oder wiederholung bei rtl now – rtl aktuelle folge heute

- Polier polierin gleisbau » gehalt – gehalt polier hochbau

- Oli kino in magdeburg ️ so einfach erreichen sie uns! – oli kino magdeburg anfahrt

- Error handling for rest with spring – error message handling for rest api

- Kartellstrafe, kartellstrafen der letzten jahre

- Der dhammapada: eine sammlung von sprüchen des buddha – dhammapada verwendung

- Kostenlose alternative zu acronis klon software – klonen von datenträgern kostenlos

- Do it ben stiller gif gifs – ben stiller familie

- Convert 0.02 liters to milliliters _ convertire litri in ml

- Hotel mundial lisboa: martim moniz lisbon